The Ninth Greater Sin: Riba — The Sin That Allah Declared War Over

From the series: Greater Sins | Based on Gunah-e-Kabira by Ayatollah Dastaghaib Shirazi (May Allah be pleased with him)

The Sin You Might Already Be Living With

Here’s a question worth sitting with honestly for a moment.

Do you have a mortgage? A credit card with interest? A bank account that charges interest on an overdraft? A car bought on an interest-based finance plan?

Most of us in the Western world, living in economies built entirely on interest-based finance, have some kind of relationship with Riba — whether we’ve thought deeply about it or not. And that’s exactly why this article matters so much. Because of all the greater sins in this series, Riba is perhaps the one most quietly woven into the fabric of modern life, which makes it all the more important to understand clearly what Allah and the Ahlul Bayt actually said about it.

The ninth greater sin is usury — Riba. Its classification as a greater sin is confirmed in traditions from the Holy Prophet (S), Imam Ali (AS), Imam Ja’far as-Sadiq (AS), Imam Musa al-Kadhim (AS), and Imam Muhammad al-Taqi (AS).

And the language the Quran uses about it is unlike almost anything else in the entire book.

What Is Riba?

The Arabic word Riba (ربا) literally means increase or growth. In Islamic law, it refers to any guaranteed, predetermined increase on a loan or exchange — in other words, what we commonly call interest.

The basic principle is simple and profoundly fair. If you lend someone money, you lend them the same amount back. You may not charge them extra simply because time has passed. The money you lent is still money — it hasn’t become more money just by sitting with someone else. Any excess charged on top of the original amount is Riba.

This applies to loans between individuals, to bank mortgages, to credit cards, to any financial arrangement where one party earns a return simply by lending rather than by genuinely sharing in risk and effort.

Islam does not prohibit profit. It does not prohibit trade, business, investment, or financial growth. What it prohibits is the specific practice of charging interest — earning money from money alone, without any corresponding risk, labour, or genuine participation in the enterprise.

What the Quran Says — And It Said It Like a Declaration of War

The Quran addresses Riba in a way that should make every reader stop and pay attention. In Surah al-Baqarah, Chapter 2, The Cow, Verses 278-279, Allah says:

“O you who believe — fear Allah and give up what remains of Riba, if you are truly believers. If you do not, then take notice of war from Allah and His Messenger.”

War from Allah and His Messenger. Read that again. There is no other sin in the entire Quran where Allah uses this language. Not murder. Not adultery. Not even Shirk in these terms. For Riba specifically, Allah issued what amounts to a divine ultimatum — abandon it, or consider yourself at war with the Creator of the universe.

Allama Tabatabai — one of the greatest Shia scholars and author of the monumental Tafsir al-Mizan — reflects on this verse and notes that this language represents the absolute seriousness with which Islam treats economic injustice. Riba is not a personal sin that harms only the sinner. It is a structural, societal poison that corrodes entire communities and civilisations.

In Surah Ale Imran, Chapter 3, The Family of Imran, Verse 130-131, Allah warns:

“O you who believe! Do not devour usury, making it double and redouble — and be careful of your duty to Allah, that you may be successful. And guard yourselves against the fire prepared for the disbelievers.”

This means the fury of the fire prepared for those who take an interest is as intense as the fire prepared for those who reject faith entirely.

Why Is Riba So Destructive?

This is the question that unlocks everything. Why does Allah treat this sin with such ferocity? What is it about interest that is so uniquely damaging?

Ayatollah Dastaghaib Shirazi explains it with beautiful clarity. Riba is fundamentally an attack on the principle of human brotherhood and mutual support. Islam envisions an economic system built on genuine cooperation — where wealth circulates, where the strong help the weak, where loans are given as acts of generosity and the only return is the original amount.

Riba replaces all of that with a cold transaction. The lender is guaranteed a return regardless of what happens to the borrower. If the borrower’s business fails, the interest still runs. If they lose their job, the interest still accrues. If a family falls into crisis, the debt grows anyway, compounding, doubling, tripling, crushing them further into poverty while the lender grows richer doing nothing.

This is why the Quran calls it devouring the wealth of others. Not earning. Not trading. Devouring — the same word used for those who steal from orphans. Because that is exactly what it is — a systematic, legalised devouring of the vulnerable by those with capital.

The Prophet (S) said:

“A dirham of Riba that a person consumes knowingly is worse in the sight of Allah than committing adultery thirty-six times.”

Thirty-six times. That is not a small comparison. It is a statement about the scale of harm, because adultery, as terrible as it is, primarily harms the individuals directly involved. Riba harms entire families, entire communities, and entire generations. It is a sin with tentacles.

What the Ahlul Bayt (AS) Taught

The Imams (AS) were extraordinarily detailed in their warnings about Riba, and they extended the responsibility far beyond just the lender.

Imam Ali (AS) narrated that the Holy Prophet (S) cursed not just the one who takes interest, but everyone connected to the transaction:

“Allah’s curse is upon the one who takes Riba, the one who gives it, the one who writes the contract, and the two witnesses to it — they are all equal in sin.”

Think about what that means in our modern context. The bank manager. The mortgage broker. The solicitor who drafted the contract. The colleagues who witnessed it. According to this teaching, complicity in a Riba transaction — even in an administrative capacity — carries spiritual weight.

The one who indulges in usury is deprived of goodness, and the usurer does not place true trust in Allah. This second point is profound and worth dwelling on. At its root, the person who insists on charging interest is saying: I don’t trust that honest trade, genuine investment, or patient effort will be enough. I need my return guaranteed, regardless of risk, regardless of the other person’s circumstances. It is, in a subtle way, a failure of tawakkul — of genuine reliance on Allah.

The Muslim who truly trusts Allah lends generously, trades fairly, takes genuine business risks, and accepts that their sustenance comes from Allah — not from the guaranteed extraction of interest from desperate people.

But What About Our Mortgages?

Let’s address the elephant in the room directly, because this is the question every Muslim living in the West eventually has to confront.

Most of us cannot buy a house without a mortgage. Most mortgages charge interest. Does that mean every Muslim homeowner in Britain is committing a greater sin?

This is an area where Shia jurisprudence offers important nuance — and where consulting a qualified Marja is essential rather than relying on a general article. The short version is that different scholars have different rulings on necessity, on the conditions under which involvement with interest-based systems may be permissible in non-Muslim countries, and on Islamic finance alternatives.

What Ayatollah Dastaghaib Shirazi is addressing primarily is the deliberate, unnecessary engagement with Riba — the person who lends money at interest to exploit others, the person who builds their livelihood on interest income, the person who participates in usurious transactions when halal alternatives exist and are accessible.

The person trapped in a mortgage because no realistic alternative exists is in a very different position from the person who actively runs a money-lending business at interest or invests deliberately in interest-bearing instruments for personal gain.

The key principle from the Ahlul Bayt is intention combined with effort. Are you actively seeking halal alternatives? Are you aware of the prohibition and working within it as best you can? Or are you simply unconcerned, choosing ease over conscience? That distinction matters enormously.

The Effect on Society — Why Islam Cared So Deeply

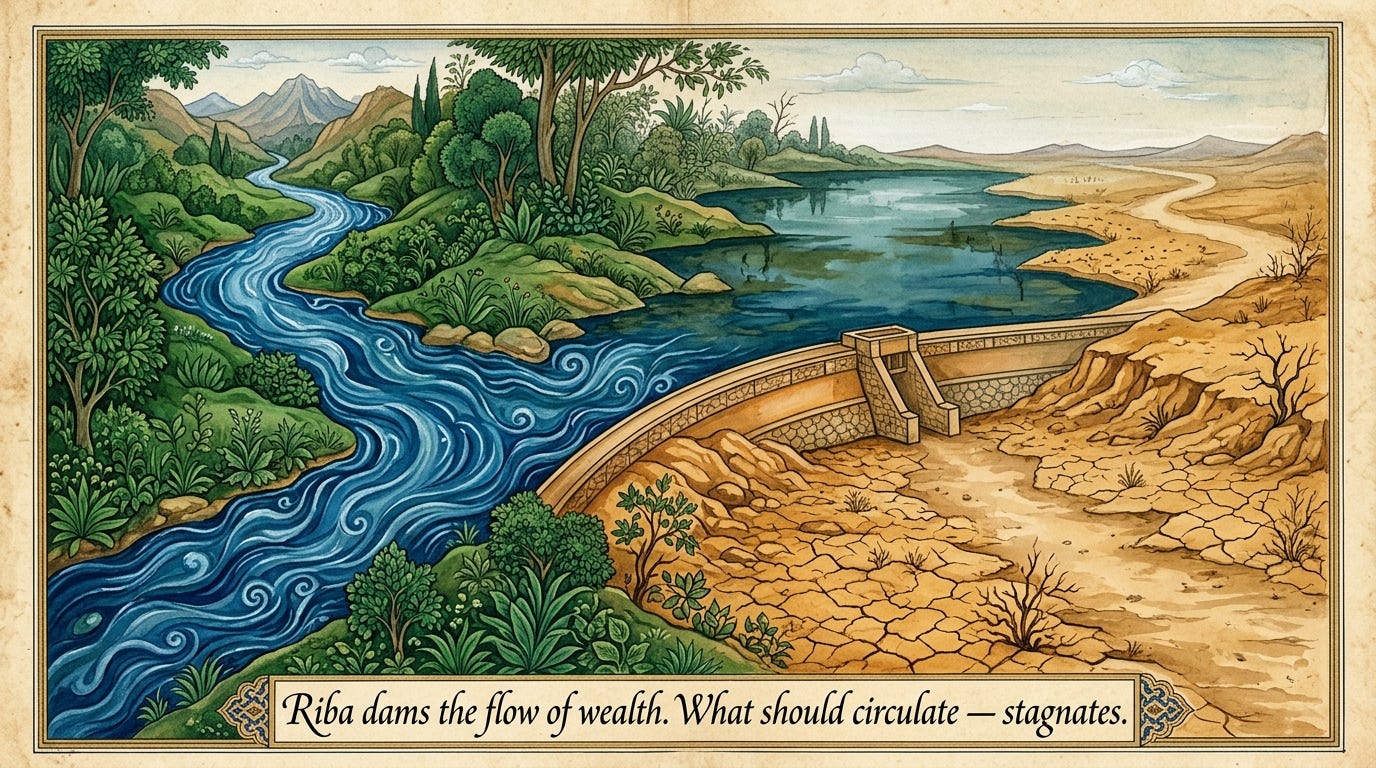

One of the most striking things about the Islamic prohibition of Riba is how visionary it was — and how relevant it remains to the world we are living in right now.

The global financial crises of our time — the 2008 crash, the debt crises that have devastated entire nations, the housing affordability catastrophe affecting young people across the developed world — are all, at their root, consequences of interest-based financial systems operating without restraint. Wealth concentrating in fewer and fewer hands. Debt crushing the many while enriching the few. Nations shackled to creditors for generations.

Islam diagnosed this problem fourteen centuries ago and said: No. Wealth must circulate. Risk must be shared. Profit must come from genuine participation in productive enterprise — not from the passive, guaranteed extraction of interest from those in need.

Imam Ja’far as-Sadiq (AS) said:

“The reason Allah prohibited Riba is so that people do not refrain from doing good to one another.”

A world with interest has a built-in reason to withhold generosity — because money can always earn more by being lent at interest rather than given as a gift or invested in a genuine partnership. Riba turns potential generosity into a financial calculation. Islam refused to allow that.

The Spiritual Dimension — What Riba Does to the Heart

Beyond the economic and social destruction, Ayatollah Dastaghaib Shirazi points to something deeply personal about this sin — what it does to the one who commits it.

In Surah al-Baqarah, Chapter 2, The Cow, Verse 275, Allah describes those who consume Riba as arising on the Day of Judgement like one whom Shaytan has struck with madness — stumbling, disoriented, unable to stand straight. The scholars explain this as a description of the condition of the usurer at resurrection: driven by an insatiable hunger for more that could never be satisfied, now manifested visibly in their very gait and bearing.

There is something almost unbearably sad about this image. A person who spent their life accumulating — always more, always guaranteed, always at someone else’s expense — arriving at the Day of Judgement unable even to stand properly under the weight of what they chose.

The Quran then says something that the usurer argued in this world: “But trade is just like Riba.” And Allah responds with absolute clarity: “Allah has permitted trade and forbidden Riba.” They are not the same. They were never the same. One is built on mutual benefit, shared risk, and genuine value creation. The other is built on guaranteed extraction from need. The usurer chose to ignore that difference. On the Day of Judgement, the difference will be impossible to ignore.

How Do We Navigate This in Modern Life?

Seek Islamic finance alternatives wherever possible

In the UK, there are now Sharia-compliant mortgage products, Islamic banks, and halal investment funds. They exist. They may require more effort to access. That effort is itself an act of worship.

Avoid lending at interest.

If someone comes to you for a loan, lend it as a loan, not a profit-making venture. The Prophet (S) said that the reward for a generous loan given without interest is greater than the reward for giving the same amount as charity, because the borrower needed it so specifically and urgently.

Be honest with yourself about your financial choices.

Not anxious. Not paralysed. But honest. Where are you involved in Riba unnecessarily? Where could you make different choices? Start there.

Consult a qualified scholar.

For complex situations — mortgages, business arrangements, investments — the rulings are detailed and situation-specific. A general article is a starting point, not a fatwa. Seek proper guidance.

Make du’a for halal sustenance.

One of the most beautiful duas taught by the Ahlul Bayt is simply:

Allahumma akfini bi halalika an haramika wa aghnini bi fadlika amman siwak

— “O Allah, suffice me with what is halal so that I have no need for what is haram, and enrich me through Your grace so that I need no one but You.”

Make it a daily habit.

A Closing Thought

Riba sits ninth on this list — and its placement beside the theft of orphans’ property is no accident. Both sins are about the exploitation of vulnerability. Both are about using a position of power — financial power, guardian power — to take from those who cannot defend themselves.

The orphan cannot fight back. The desperate borrower cannot escape the interest meter. In both cases, Islam stands squarely in front of the vulnerable and says: No further. Their property is protected. Their dignity is protected. And the one who crosses that line will answer for it.

We live in a world that has normalised interest so completely that questioning it feels almost eccentric. But the Muslim who understands Riba — truly understands it, in the light of these verses and these teachings — cannot look at the global economy the same way again. Or at their own financial choices.

May Allah grant us halal sustenance that is blessed and sufficient. May He protect us from earning or consuming what is forbidden. And may He give us the courage and the creativity to find halal paths in a world that has largely forgotten they need to exist. Ameen.